The types of bank accounts you can open depend on your bank, but the most common options are:

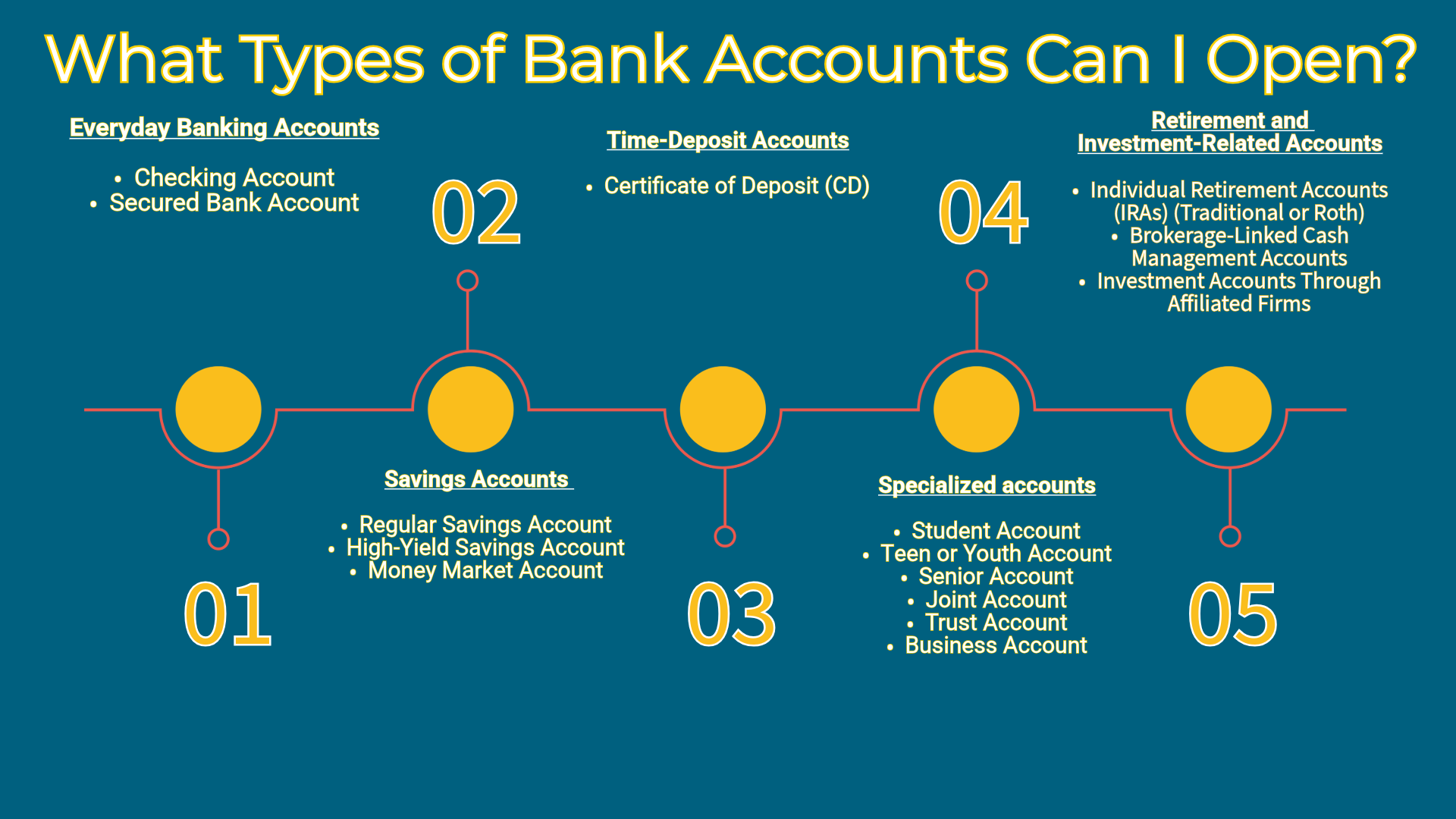

Everyday Banking Accounts

- Checking account

- Designed for daily spending, bill payments, check-writing, and direct deposits.

- Usually includes a debit card and online banking in addition to check-writing privileges.

- Secured account (not all banks offer them)

- A simplified account with fewer features and lower fees.

- Designed to deposit money and withdraw money tied to the balance in the account (no check-writing or overdrafts.)

- Often intended for people who are new to banking or rebuilding their finances.

Savings Accounts

- Regular savings account

- Earns interest on your money while keeping it accessible.

- May limit certain types of withdrawals.

- High-yield savings account

- Typically offers higher interest rates than traditional savings accounts.

- Often available through online banks.

- Money market account

- Usually pays competitive interest rates.

- May include limited check-writing or debit card access.

Time-Deposit Accounts

- Certificate of Deposit (CD)

- You agree to keep money deposited for a fixed term (such as 6 months, 1 year, or 5 years).

- Usually pays a higher interest rate than a standard savings account.

- Early withdrawals often incur penalties.

Specialized Accounts

- Student account

- Designed for students and may have reduced fees or minimum balance requirements.

- Teen or youth account

- Often opened jointly with a parent or guardian.

- Senior account

- May offer benefits tailored to older adults.

- Joint account

- Shared by two or more account holders, commonly spouses or family members.

- Trust account

- Managed according to the terms of a legal trust.

- Business account

- Used for business income and expenses.

- Available for sole proprietors, LLCs, corporations, and other business types.

Retirement and Investment-Related Accounts

In the United States, banks and financial institutions may also offer:

- Individual Retirement Accounts (IRAs) (Traditional or Roth)

- Brokerage-linked cash management accounts

- Investment accounts through affiliated firms

What You'll Usually Need

To open an account in the U.S., banks typically ask for:

- Government-issued photo ID

- Social Security Number or Taxpayer Identification Number (if applicable)

- Proof of address

- Initial deposit

How You’re Protected

-

The Federal Deposit Insurance Corporation (FDIC) was created in 1933 following the bank runs of the Great Depression. This independent agency of the U.S. government maintains stability and public confidence in the nation’s financial system.

-

The FDIC’s primary mandate is to insure deposits held in commercial banks and savings associations. These insured institutions display the official FDIC sign. The agency monitors the financial health of over 4,000 banks and savings associations across the country.

-

A single account is insured up to $250,000. If that person also holds a joint account with a spouse at the same institution, the joint account is separately insured up to $500,000, as each co-owner receives $250,000 coverage.

COMING NEXT WEEK: CREDIT UNION ACCOUNTS!