Choosing between a debit card and a credit card comes down to how you manage money, your goals, and your tolerance for risk. Here’s a breakdown of the pros and cons of each:

Debit Card

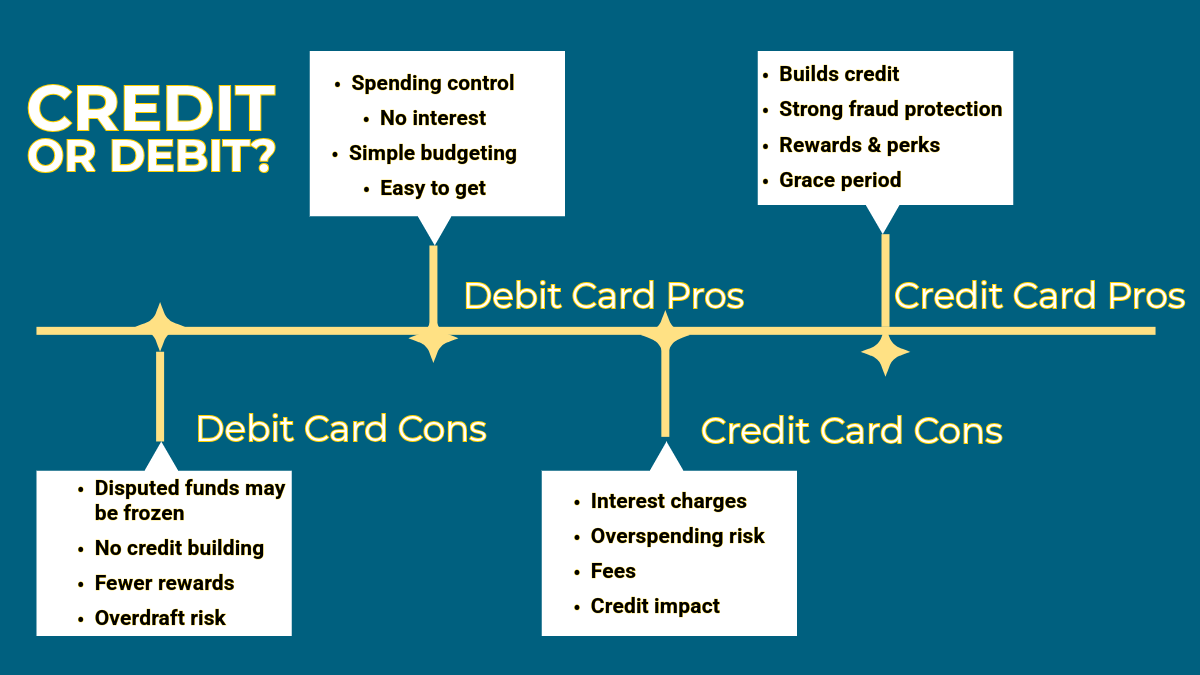

Pros

- Spending control: You can only spend what’s in your bank account, which helps avoid debt.

- No interest charged: Since you’re using your own money, there are no interest charges. Some banks and credit unions pay interest for idle funds held in a debit card account.

- Simple budgeting: Transactions come out immediately, making it easier to track spending.

- Easy to get: No credit check required.

Cons

-

Problems may result in the amount in dispute being frozen until final resolution.

- No credit building: Debit cards don’t help build your credit history.

- Fewer rewards: Rarely offer cashback, points, or travel perks.

- Overdraft risk: If you overspend, you might face overdraft fees.

Credit Card

Pros

- Builds credit: Responsible use helps improve your credit score.

- Strong fraud protection: Easier to dispute charges without losing your own money upfront.

- Rewards & perks: Many cards offer cashback, travel rewards, or purchase protections.

- Grace period: You can delay payment without interest if you pay your balance in full each month.

Cons

- Interest charges: Carrying a balance can lead to high-interest debt.

- Overspending risk: Easy to spend more than you actually have.

- Fees: Some cards have annual fees, late fees, or foreign transaction fees.

- Credit impact: Missed payments or high balances can hurt your credit score.

When to Use Each

Debit card is better if:

- You want strict spending discipline

- You’re avoiding debt entirely

-

You’re managing a tight budget

Credit card is better if:

- You pay your balance in full every month

- You want to build credit

- You want rewards

Bottom line

- Debit is safer for budgeting, but fewer benefits

- Credit is more powerful financially, but requires discipline